A Convergent Economy

By the Numbers (Year-to-Date)*

U.S. Equities (S&P 500 Index) | 13.4%

International Equities (MSCI ACWI ex-U.S.) | 5.0%

U.S. Bonds (Barclays U.S. Aggregate Bond Index) | 7.4%

Global Bonds (JP Morgan Global Aggregate Bond Index) | 7.8%

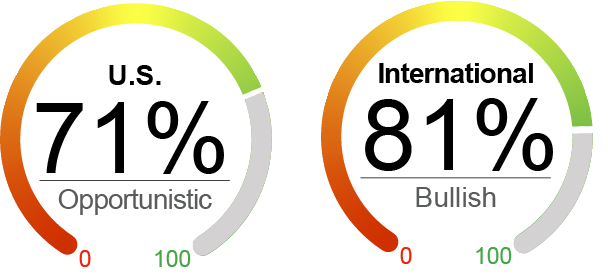

The NorthCoast Navigator is a market barometer displaying NorthCoast's current U.S. equity outlook. This aggregate metric is determined by multiple data points across four broad market-moving dimensions: Technical, Sentiment, Macroeconomic, and Valuation. The daily result determines equity exposure in our tactical strategies.

As of 11/30/2020. Data provided by Bloomberg, RBC, NorthCoast Asset Management.

*Source: Bloomberg, NorthCoast Asset Management.

|

Negative Indicator |

Neutral Indicator |

Positive Indicator |

Positive Indicator |

|

Valuation The market gains in November pushed valuation indicators more negative than the prior month. The rotation into value stocks are pushing those valuations higher but they are still at more attractive entry points than growth stocks. P/E ratio rose to 28.4 from 25.8. |

Sentiment Sentiment regarding equities and economic activity certainly jumped in November off of vaccine news. However, consumer sentiment actually weakened according to the University of Michigan Consumer Sentiment survey. This negative change reflects the immediate reality of increasing Covid-19 cases. |

Technical Technical indicators remained relatively steady compared with the end of October. While momentum turned positive and the S&P 500 sits well above its moving averages, reversal indicators are flashing orange and red after such a steep run-up. Volatility did calm thanks to the election seemingly confirmed and certainly the vaccine news. |

Macroeconomic Data released in November showed that consumer spending grew in October by a modest 0.5%. Below September’s growth rate, it still shows the economy recovering from springtime losses. The uptick in cases however, has led to increasing jobless claims and worry of lockdowns prior to vaccine distribution. Forecasts show slowing growth in Q4.

|

Important Disclosures

The information contained herein has been prepared by NorthCoast Asset Management LLC (“NorthCoast”) on the basis of publicly available information, internally developed data and other third party sources believed to be reliable. NorthCoast has not sought to independently verify information obtained from public and third party sources and makes no representations or warranties as to accuracy, completeness or reliability of such information. All opinions and views constitute judgments as of the date of writing without regard to the date on which the reader may receive or access the information, and are subject to change at any time without notice and with no obligation to update. This material is for informational and illustrative purposes only and is intended solely for the information of those to whom it is distributed by NorthCoast. No part of this material may be reproduced or retransmitted in any manner without the prior written permission of NorthCoast. NorthCoast does not represent, warrant or guarantee that this information is suitable for any investment purpose and it should not be used as a basis for investment decisions. © 2020 NorthCoast Asset Management LLC.

PAST PERFORMANCE DOES NOT GUARANTEE OR INDICATE FUTURE RESULTS.

This material should not be viewed as a current or past recommendation or a solicitation of an offer to buy or sell any securities or investment products or to adopt any investment strategy. The reader should not assume that any investments in companies, securities, sectors, strategies and/or markets identified or described herein were or will be profitable and no representation is made that any investor will or is likely to achieve results comparable to those shown or will make any profit or will be able to avoid incurring substantial losses. Performance differences for certain investors may occur due to various factors, including timing of investment. Investment return will fluctuate and may be volatile, especially over short time horizons.

INVESTING ENTAILS RISKS, INCLUDING POSSIBLE LOSS OF SOME OR ALL OF AN INVESTMENT.

The investment views and market opinions/analyses expressed herein may not reflect those of NorthCoast as a whole and different views may be expressed based on different investment styles, objectives, views or philosophies. To the extent that these materials contain statements about the future, such statements are forward looking and subject to a number of risks and uncertainties.